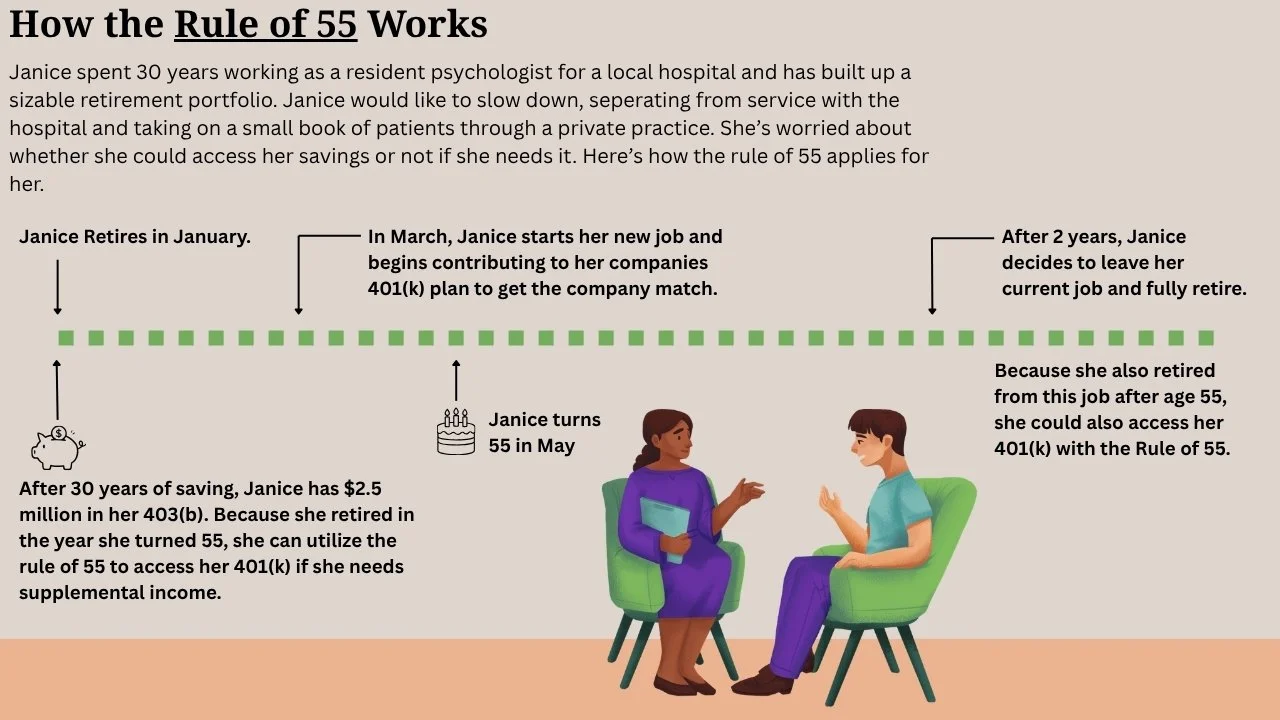

The Rule of 55: How to Access Your 401(k) Before Age 59½ Without the 10% Penalty

"I'm 55, ready to retire, but all my savings are in 401(k)s and IRAs. Do I have to wait until age 59½ to access my money without paying a penalty?"

Fortunately, not always.

There is an IRS provision known as the Rule of 55 that allows certain individuals to take penalty-free withdrawals from a former employer's 401(k) or 403(b) plan before age 59½ under specific circumstances.

In this article, I'll explain how the Rule of 55 works, who qualifies, and several common situations where it can be a valuable retirement planning strategy.

What Is the Rule of 55?

The Rule of 55 allows individuals to take penalty-free withdrawals from an employer-sponsored retirement plan, such as a 401(k) or 403(b), if they separate from service with that employer during or after the calendar year in which they turn age 55.

Normally, withdrawals from retirement accounts before age 59½ are subject to a 10% early withdrawal penalty, in addition to ordinary income taxes. The Rule of 55 waives only the 10% penalty. Withdrawals are still generally subject to ordinary income tax.

It is important to understand that this provision does not apply to IRA accounts or to 401(k) or 403(b) plans from previous employers. It only applies to the retirement plan sponsored by the employer from whom you separated during or after the year you turned 55.

Who Qualifies for the Rule of 55?

Generally, you may qualify if:

You leave your employer during or after the calendar year you turn 55.

The assets remain in that employer's qualified retirement plan.

Your employer's retirement plan permits withdrawals after separation from service.

If your employer's plan does not allow distributions after separation, you may not be able to utilize the Rule of 55 until the plan permits withdrawals.

Things to Consider Before Using the Rule of 55

1. Understand Your Plan's Distribution Rules

Although the IRS allows penalty-free withdrawals under the Rule of 55, your employer's retirement plan determines how distributions are handled.

Some plans allow flexible partial withdrawals, while others require participants to withdraw the entire balance once distributions begin.

If your plan requires a lump-sum distribution, you could unintentionally create a significant taxable event.

Before making any decisions, review your plan's distribution options with your plan administrator.

2. Roth 401(k) Withdrawals May Still Have Tax Consequences

If your retirement savings are held in a Roth 401(k), the Rule of 55 still eliminates the 10% early withdrawal penalty.

However, earnings may still be taxable if the distribution is not considered a qualified Roth distribution. Generally, qualified distributions require:

The Roth account to have satisfied the five-year holding period, and

The participant to be age 59½, disabled, or deceased.

Because the Rule of 55 only waives the penalty—not the Roth qualification rules—it's important to understand the tax implications before taking distributions.

Click here to get your FREE electronic copy of: Fiduciary - How to Find, Hire, and Establish an Aligned Trusted Partnership with a Fee-Only Financial Advisor

3. You Can Return to Work

Many people assume they cannot work again after using the Rule of 55.

Fortunately, that isn't true.

If you retire under the Rule of 55 and later accept another job, you may continue taking penalty-free withdrawals from your former employer's retirement plan while also participating in your new employer's retirement plan.

The key requirement is that the funds remain in the retirement plan of the employer from whom you originally separated.

4. Consider the Long-Term Impact on Your Retirement

Just because you can access your retirement savings early doesn't necessarily mean you should.

Large withdrawals early in retirement reduce the amount of money remaining in your portfolio to grow through compounding.

The earlier distributions begin, the greater the potential impact on the long-term sustainability of your retirement assets.

Before relying on the Rule of 55, it's wise to project how various withdrawal strategies may affect your retirement over the next 25 to 35 years.

When Does the Rule of 55 Make Sense?

The Rule of 55 can be an excellent planning tool for individuals who need to bridge the gap between early retirement and other income sources.

Here are several common scenarios where it may be beneficial.

Scenario 1: Unexpected Job Loss

Mike is 57 when his employer downsizes and eliminates his position.

Although he originally planned to work until age 60, he now needs income while deciding whether to retire or pursue another career.

Rather than paying the 10% early withdrawal penalty, Mike can use the Rule of 55 to access his former employer's 401(k) penalty-free.

Scenario 2: Waiting for a Pension

David retires from a private company at 56, but his pension doesn't begin until age 60.

He uses the Rule of 55 to take distributions from his 401(k), allowing him to bridge the four-year gap until his pension payments begin.

Scenario 3: Semi-Retirement

Emily decides to leave her corporate career at 55 and transition into part-time consulting.

Although her consulting income covers part of her living expenses, she supplements the remainder with penalty-free withdrawals from her former employer's 401(k).

This allows her to enjoy semi-retirement while delaying full retirement.

Give Your Kids A Head Start on Retirement With A Trump Account — Click here to learn more

Advantages of the Rule of 55

The Rule of 55 can provide several important benefits:

Access retirement savings before age 59½ without the 10% penalty.

Bridge the income gap between retirement and Social Security or pension benefits.

Increase flexibility for individuals pursuing semi-retirement.

Provide income after an unexpected layoff or early retirement.

Potentially avoid higher-interest debt during temporary income shortages.

Potential Drawbacks

Despite its advantages, the Rule of 55 isn't appropriate for everyone.

Potential disadvantages include:

Withdrawals remain subject to ordinary income tax.

Larger withdrawals may increase your tax bracket.

Early distributions reduce future investment growth.

Not every employer plan offers flexible withdrawal options.

The rule does not apply to IRA accounts.

Illustration used for educational purposes — It is recommended that you contact a CPA or Financial Professional to discuss your specific circumstances.

Final Thoughts

The Rule of 55 can be an incredibly valuable retirement planning strategy for individuals who retire earlier than expected or simply want greater flexibility before age 59½.

However, accessing retirement savings early should never be viewed as a standalone decision. The amount withdrawn, the timing of withdrawals, taxes, future investment growth, and your overall retirement income strategy all need to be carefully coordinated.

Before using the Rule of 55, consider working with a qualified financial advisor to evaluate how early withdrawals may impact the longevity of your retirement assets and determine whether this strategy fits into your overall retirement plan.

With proper planning, the Rule of 55 can serve as an effective bridge to retirement while helping you avoid unnecessary IRS penalties.

As always have a wonderful day,

a better weekend,

and I look forward to writing to you next Friday!

Written by Ryan Morrissey CFP®, CLU®, CHFC®, CMFC

Founder & Principal Advisor of Morrissey Wealth Management

Host of the Retire with Ryan Podcast

_____________________________________________________________________________________________

Frequently Asked Questions

Can I use the Rule of 55 with an IRA?

No. The Rule of 55 only applies to eligible employer-sponsored retirement plans such as 401(k)s and 403(b)s. It does not apply to Traditional or Roth IRAs.

Do I still pay income tax on Rule of 55 withdrawals?

Yes. The Rule of 55 eliminates the 10% early withdrawal penalty, but distributions are generally still subject to ordinary income tax.

Can I roll my 401(k) into an IRA and still use the Rule of 55?

No. Once the funds are rolled into an IRA, they generally lose eligibility for the Rule of 55 exception.

Can I continue working after using the Rule of 55?

Yes. You may accept employment with another company and continue taking penalty-free withdrawals from your former employer's retirement plan, provided the assets remain in that plan.