5 Questions To Ask Yourself Before You Retire

There are many factors that come together to determine if someone is ready for retirement. While financial preparedness is often at the forefront, there are a number of other topics one must consider to ensure they understand how they want to spend their golden years—and can quantify how much they’ll need to make it happen.

In this article, I will cover 5 crucial questions you should be able to answer when planning for retirement. Please keep in mind, these are just 5 of the many questions we walk our clients through during a financial planning engagement. However, these 5 will help you develop a solid understanding of what retirement looks like for you—and what it might take to make that vision a reality.

1.What Does My Ideal Retirement Look Like?

This may seem like a broad place to begin—and you’re right. That’s the point. Every person is unique and has a vastly different vision for how they plan to spend their retirement.

Some want to buy a sail boat and travel the world, others want to make large charitable contributions to their communities, and many consider making large gifts to their children and grandchildren to help pay for higher education, first homes, weddings, and more.

The point is, if we don’t understand the “why,” how can we possibly answer the “how”?

From this understanding, we can begin by determining your foundation — Your current living expense needs.

It is crucial to construct—and regularly update—a budget so you have a clear understanding of what it would cost, on both a monthly and annual basis, to sustain your current lifestyle.

Will There Be Any Changes Once I Retire?

Are there expenses that will fall off upon retirement?

Perhaps you’re in the final years of your mortgage, planning to downsize your home, or you will have your vehicles paid off soon. Maybe you’ll no longer be paying a large annual membership or club fees.

All of these considerations will help refine your budget and determine how much you’ll actually need to fund your retirement.

How Will Larger One-Off Expenses Affect My Retirement Cash Flow?

Planning for larger, one-time expenses is equally important.

For those who who find the thought of spreadsheets and cash flow projections to be overwhelming, it may be beneficial to sit down with a financial advisor who can develop a model based on your expected retirement income, ongoing living expenses, and anticipated one-off expenses.

This type of analysis can provide clarity on how these additional expenses may impact the longevity of your retirement—and how much you may need to save to ensure they don’t.

2.How Much Do I Need to Save to Retire?

This is a highly subjective question. Every person has a different vision of retirement and varying levels of expenses that must be covered by different sources of income.

For example, let’s say a client—Sammy—determines that she needs $100,000 annually, after taxes, to support her retirement lifestyle.

Does It All Come From My IRA / 401(k) / 403(b)?

It’s important to account for all potential income sources—such as Social Security benefits, pension income, real estate income, etc., to determine how much will need to be supplemented through withdrawals from retirement accounts.

Let’s assume Sammy is 67 years old, single, and has:

A pension that pays $1,000 per month ($12,000 annually)

Social Security income of $2,500 per month ($30,000 annually)

In this scenario, Sammy has $42,000 of her income covered. She would need to generate the remaining $58,000 from her portfolio—plus enough to cover applicable income taxes, especially if none is being withheld from her pension or social security.

For this example, let’s assume that her total withdrawal need comes to $75,000 annually.

A simple way to estimate a conservative amount needed to support this level of withdrawals is to divide the annual withdrawal by 4%:

$75,000 ÷ 0.04 = $1,875,000

While it’s very possible that Sammy could sustain her retirement with less saved, this calculation reflects the 4% withdrawal rule, which is considered a conservative guideline to help mitigate the risk of outliving retirement savings over a 30-year period. Many advisors suggest withdrawal rates can be closer to 4.7%, and more subscribe to a dynamic withdrawal approach that allows even higher rates of distribution, however these strategies accompany strict guidelines for income reduction in the event of a market decline.

Click here to listen to my podcast episode — with colleague Matthew Jarvis, where we discussed utilizing the dynamic guardrail withdrawal strategy to get more income in retirement!

Click here to get your FREE electronic copy of: Fiduciary - How to Find, Hire, and Establish an Aligned Trusted Partnership with a Fee-Only Financial Advisor

3. When Should I Begin Collecting Social Security?

While you can begin collecting Social Security as early as age 62, you should understand how much this decision may reduce your benefit.

For individuals born in 1960 or later, choosing to begin collecting benefits at age 62 will result in a permanent 30% reduction in your monthly benefit. The Social Security Administration reduces benefits based on how many months before your full retirement age (FRA) you begin collecting.

Benefits are reduced by:

5/9 of 1% per month for the first 36 months before FRA

5/12 of 1% per month for any additional months beyond that

Example: Early Claiming Reductions (FRA = 67)

12 months early → 6.67% reduction

24 months early → 13.33% reduction

36 months early → 20% reduction

48 months early → 25% reduction

60 months early → 30% reduction

What If You’re Still Working?

If you plan to collect early while still working, you also need to consider the earnings test.

If your income exceeds the annual limit (currently $24,480 and adjusted annually), your benefits may be reduced:

Before FRA: $1 withheld for every $2 earned above the limit

In the year you reach FRA: $1 withheld for every $3 earned above the limit

For those who expect to continue working until age 67, it often doesn’t make sense to claim early. You may lock in a reduced benefit while also having a portion of that benefit withheld due to the earnings test.

Should I Delay Collecting Beyond My FRA?

This is another important question—and one that should be carefully evaluated.

For each year you delay collecting Social Security beyond your FRA (up to age 70), your benefit increases by 8% annually.

👉 Delaying from age 67 to 70 can increase your benefit by approximately 24%.

Whether this strategy makes sense depends on your individual situation, including:

Your health and life expectancy

Your employment status

Your ability to cover expenses from other income sources

I recommend evaluating whether you can support your lifestyle without Social Security and running a break-even analysis to determine the age at which delaying results in greater total lifetime benefits.

How Do COLAs Affect My Benefit?

Another key factor to understand is how Cost-of-Living Adjustments (COLAs) impact your benefit.

Whether you claim at 62 or delay until 70, COLAs are applied equally as a percentage. However:

Claim early → COLAs apply to a smaller base benefit

Delay → COLAs apply to a larger base benefit

This is why delayed benefits can grow significantly larger over time—the increases compound on a higher starting amount.

4. How Will Taxes Impact My Retirement?

Many retirees are surprised by how important tax planning is in retirement.

Carefully structuring your income—and understanding how each source is taxed—can help ensure you are not:

A. Surprised when you file your taxes

B. Paying more in taxes than necessary

How Retirement Income Is Taxed

At a high level, here’s how common income sources are treated:

Pre-tax retirement accounts—such as traditional IRAs, 401(k)s, 403(b)s, 457 plans, Thrift Savings Plans, SEP IRAs, and SIMPLE IRAs—are taxed as ordinary income when withdrawn.

Additionally, withdrawals taken before age 59½ are generally subject to a 10% early withdrawal penalty, on top of ordinary income taxes. This can significantly impact the longevity of your portfolio, so careful planning is essential before taking early distributions.

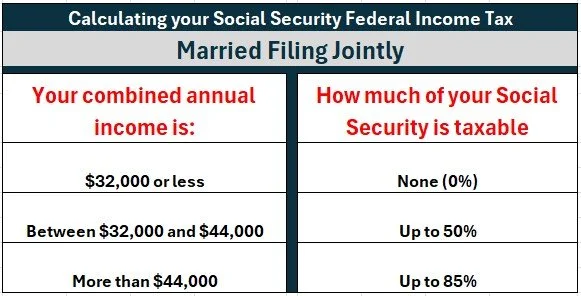

Is Social Security Taxable?

Despite common misconceptions, Social Security can be taxable.

The key question is: how much is taxable?

That depends on your total household income, whether you are filing as a single individual or married couple.

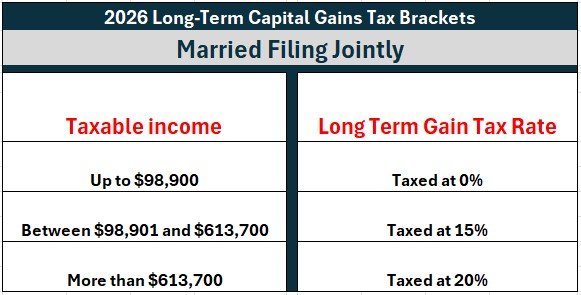

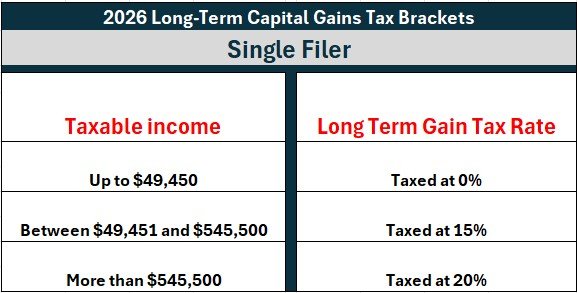

Pension income is subject to ordinary income tax rates. Investments held in a taxable brokerage account are subject to short-term capital gains tax rates if the position is held for less than 12 months—these gains are taxed as ordinary income.

For long-term capital gains, which apply to positions held for 12 months or more, the gains are taxed at more favorable rates.

And withdrawals taken from a Roth IRA are 100% tax-free. However, distributions of earnings from a Roth IRA prior to reaching age 59½ may be subject to a 10% early withdrawal penalty if certain conditions are not met.

All of this is to say—it is very important to carefully plan where and when you take withdrawals to cover your retirement expenses. Improper planning can cause you to miss opportunities to minimize your lifetime tax exposure and may result in paying more in taxes than necessary in a given year.

5. Have I Properly Planned for Health Care Expenses and LTC?

For many retirees, they’ve spent years benefiting from employer-sponsored group health and life insurance policies at reduced costs. However, once retired, they become responsible for securing their own coverage—whether through Medicare at age 65 or by navigating the individual health insurance market, which can come with aggressive ACA subsidy cliffs prior to Medicare eligibility.

Healthcare is often one of the primary reasons many individuals choose to continue working until at least age 65, allowing them to transition directly from an employer-sponsored plan to Medicare.

Additionally, Medicare is not free, despite common misconceptions. While Medicare Part A is typically premium-free for most retirees, Medicare Part B and Part D (prescription drug coverage) come with monthly premiums. If you’d like a more in-depth explanation of how Medicare works, your available options, and associated costs, you can read my article: Medicare Explained at 65: Parts A, B, C, D, Costs & Enrollment Timing.

Beyond traditional health insurance, it’s important to think ahead and consider the potential need for long-term care for you or your spouse. A financial advisor can help project the impact a long-term care event may have on the longevity of your retirement assets—whether that involves the cost of an in-home health aide or transitioning to an assisted living facility.

While it may feel uncomfortable to think about these possibilities, it’s an important discussion to have so you understand where you stand if the situation becomes a reality. For some, their portfolios and retirement cash flow may be sufficient to cover these expenses. For others, it may make sense to explore long-term care insurance as a way to mitigate this risk.

To assist in assessing these costs — You can click here — to be directed to a tool that estimates long-term care costs based on your location. These tools allow you to input your ZIP code, apply a reasonable inflation assumption, and compare projected costs for in-home care, assisted living, and other long-term care options.

Final Thoughts

As I mentioned in the beginning of this article, these are just 5 of the many questions that someone should be able to answer before they transition into retirement. I hope this gave you something to think about, and I encourage you to reach out if you feel you’d like professional help developing a custom tailored and comprehensive plan for your retirement.

As always have a wonderful day,

a better weekend,

and I look forward to writing to you next Friday!